Royalty Interest

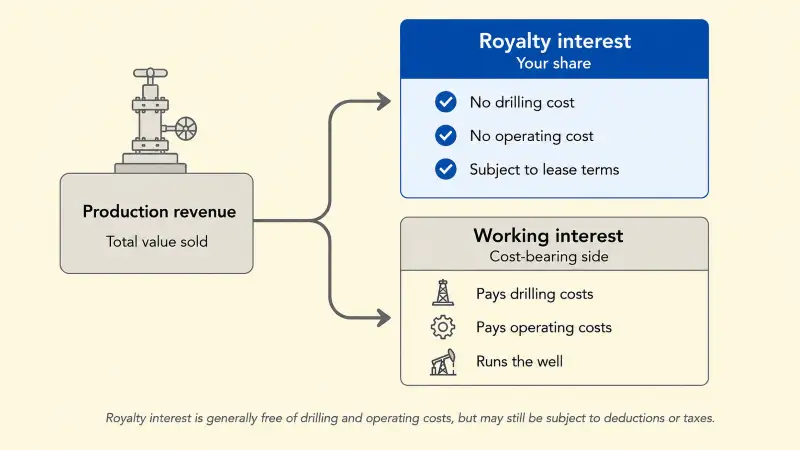

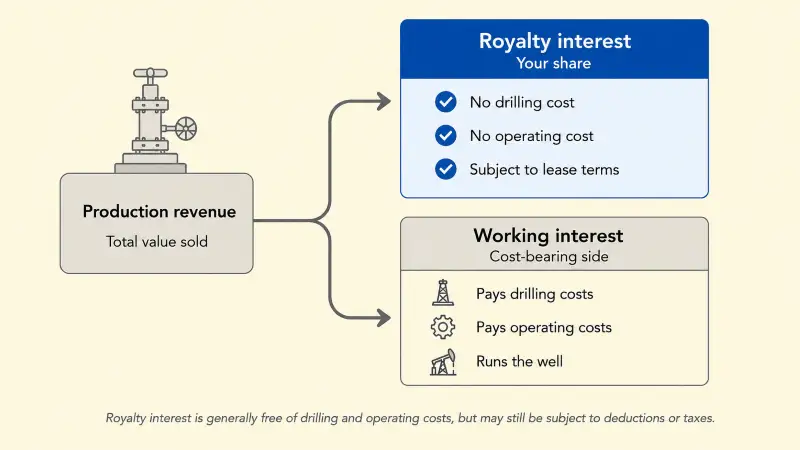

A royalty interest is your right to a share of the revenue from an oil and gas property, generally without paying any of the costs to drill, operate, or plug the wells.

For most mineral owners, the royalty interest is the heart of what they hold once they lease their minerals: the lessee, meaning the company that leased your minerals, and the other working interest owners take on the costs and risks of drilling and operating the wells, while you receive a cost-free share of production revenue.

It is usually written as a fraction or decimal, such as one-eighth, three-sixteenths, or one-quarter, and that figure helps determine the size of your royalty checks.

What This Means for Mineral Owners

If you leased your minerals and receive royalty checks, you likely hold a lessor's royalty, which is one common type of royalty interest. It is the lease-based interest that turns production into income for the mineral owner. The defining feature, and the reason it is valuable, is that it is generally free of drilling, completion, operating, and plugging costs. You generally do not pay to drill, complete, operate, work over, or plug the well. The working interest owners carry those costs, and you receive your royalty share of production revenue.

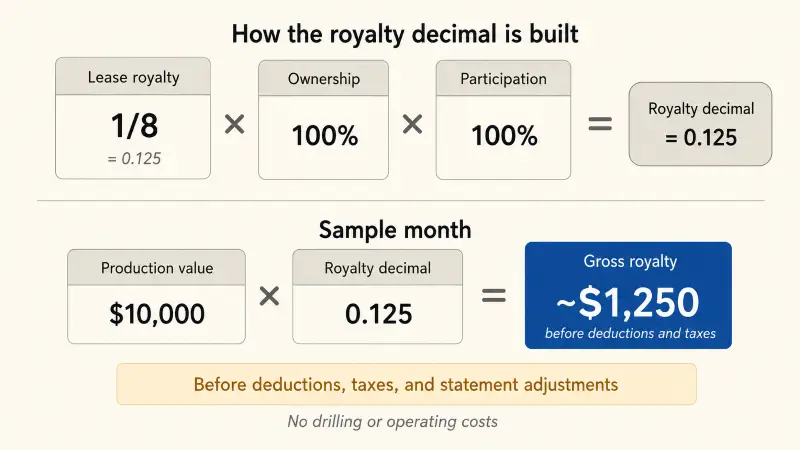

A simple way to think about it is that your ownership share, your tract or unit participation, and your lease royalty fraction together produce your royalty decimal interest, which is the share applied to your payments on the division order or royalty statement.

A royalty interest is generally cost-free as to drilling and operating costs, but it is not always free of post-production deductions, taxes, or other statement-level adjustments. Depending on your lease language and the valuation point for royalty, post-production costs such as gathering, compression, dehydration, treating, processing, transportation, and marketing-related charges may be subtracted from your share. These are different from drilling and operating costs.

The royalty fraction in your lease is generally set when the lease is signed. While that lease remains validly in force, the royalty fraction generally does not change unless the lease is amended or a specific lease provision changes the result.

How a Royalty Interest Works

When you lease your minerals, you grant the lessee the right to explore for, drill, and produce oil and gas under the lease terms, and in exchange you reserve a royalty for yourself. From that point on, the working interest owners fund the wells, the operator manages operations, and you hold a generally cost-free claim on a portion of production revenue.

The royalty fraction and your decimal

The lease states a royalty fraction, such as one-eighth, three-sixteenths, one-fifth, or one-quarter. One-eighth was the traditional standard for many years, while many modern Texas leases are negotiated at higher fractions such as three-sixteenths or one-quarter, so an older inherited lease may carry a lower fraction than newer leases in the same area. Your royalty decimal takes that fraction and adjusts it for your mineral ownership, tract participation, unit participation, and any other title or allocation factors used to calculate payment.

Ownership share × tract or unit participation × lease royalty fraction = royalty decimal

The larger your ownership share and the higher your royalty fraction, the larger your decimal usually is, and the larger your checks may be for a given level of production, price, and deductions.

Cost-free, but watch post-production costs

The cost-free nature of a royalty interest generally applies to drilling, completion, operating, workover, and plugging costs. It does not always extend to costs incurred after production, such as gathering, compression, dehydration, treating, processing, transportation, or marketing-related costs. Whether those post-production costs can be deducted from your share depends on your lease wording, the royalty valuation point, any no-deductions language, and how Texas courts interpret those provisions. This is one of the more contested areas of Texas royalty accounting.

A worked example

Suppose your lease reserves a one-eighth, or 0.125, royalty, and you own all the minerals in the tract or producing unit used for this simple example. If production attributable to your interest sold for $10,000 in a month, your gross royalty would be about $1,250 before any post-production deductions, severance taxes, ad valorem taxes, payment thresholds, or other statement-level adjustments. You generally would owe nothing toward the cost of drilling, completing, operating, working over, or plugging the well.

The figure is illustrative, but it shows the basic way a royalty fraction converts production value into gross royalty income before deductions, taxes, and other adjustments.

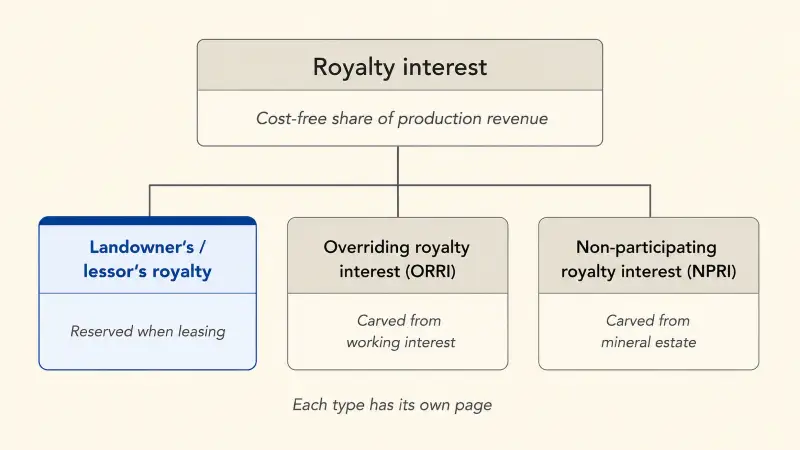

Types of Royalty Interest

Royalty interest is the broad category. Several specific types fall under it, and each has its own page:

- Landowner's or lessor's royalty: the royalty a mineral owner reserves when leasing minerals. This is the type most leased mineral owners hold.

- Overriding royalty interest: a cost-free royalty carved from the working interest in a specific lease, which usually ends when that lease ends.

- Non-participating royalty interest: a royalty interest carved from the mineral estate that usually does not include executive leasing rights, bonus rights, or delay rental rights, and may continue across leases depending on the deed or instrument.

Royalty Interest vs Working Interest

The clearest way to understand a royalty interest is to contrast it with the interest that bears the costs.

| Royalty interest | Working interest | |

|---|---|---|

| Pays drilling and operating costs | No | Yes |

| Receives a share of revenue | Yes, generally free of drilling and operating costs | Yes, after royalties and costs |

| Controls operations | No | Yes |

| Typical holder | Mineral owner, lessor, royalty owner, NPRI owner, or ORRI owner, depending on the interest type | Working interest owner, operator, or investor |

The cost-bearing side is the working interest, and the operator is the party designated to manage operations for the working interest owners. One related figure worth distinguishing is net revenue interest, or NRI. It often describes a working interest owner's net share of revenue after royalty burdens, while mineral owners usually focus on the royalty decimal shown on the division order or royalty statement.

Why Your Royalty Interest Matters

Your royalty interest is the main engine of your mineral income after your minerals are leased and production is sold. Because it is generally free of drilling and operating costs, a royalty interest does not require you to pay for dry holes, drilling costs, completion costs, workovers, or plugging costs. However, a dry hole or underperforming well can still affect whether you receive future royalty income. At the same time, the size of your actual check is shaped by your royalty fraction, ownership share, decimal interest, production volumes, realized prices, product mix, severance taxes, post-production deductions, payment thresholds, and lease terms.

It also helps to know that the royalty fraction is generally fixed once you have leased. While a lease remains validly in force, you generally cannot raise your royalty rate unless the lease is amended or a new lease is signed after the existing lease ends or releases the relevant rights.

For owners who want to see how their royalty interest may perform as income over time, Mineral View's MVestimate models projected royalty income using production data, decline behavior, product mix, and price assumptions.

A Real-World Scenario

Example: Patricia's inherited royalty interest in Karnes County

Patricia inherited a royalty interest tied to a producing lease in Karnes County, Texas. She knew she received royalty checks but had never been clear on what type of interest she owned, how her decimal was calculated, or why her checks were smaller than she expected based on the well's production.

When she looked closely, two things became clear. First, her interest was generally free of drilling and operating costs, so she was not being charged for drilling, completion, workover, or operating expenses. Second, her lease appeared to allow certain post-production costs to be deducted, which helped explain part of the gap between gross production revenue and her net check.

Understanding that she held a royalty interest free of drilling and operating costs, while still possibly subject to post-production deductions, helped Patricia read her statements with more confidence and ask better questions about the specific deductions.

Note: This example is provided for illustrative purposes only and does not represent any specific mineral owner or lease.

What to Check

Confirm your royalty fraction, ownership share, and decimal

Your lease states the royalty fraction, and your division order or royalty statement usually shows the decimal applied to your payments. A division order generally reflects your existing royalty and ownership for payment purposes rather than setting or changing the royalty fraction in your lease, so it is worth confirming the decimal matches your lease and ownership before signing. Knowing the royalty fraction, your ownership share, the producing tract or unit, and your decimal is the foundation for understanding whether your payments look reasonable.

Check whether post-production costs are being deducted

Cost-free refers mainly to drilling, completion, operating, workover, and plugging costs. Post-production costs, severance taxes, and other statement-level adjustments are separate matters governed by your lease, product sales, and applicable law. Reviewing your statements for deductions, taxes, and price adjustments, and reviewing your lease for what it allows, helps you understand whether the gap between gross revenue and your check is expected.

Mineral View's Monthly Report summarizes revenue trends across your minerals over time, which can make deduction patterns easier to spot than reading one statement at a time.

Understand what type of royalty you hold

Most leased mineral owners hold a landowner's or lessor's royalty, but some owners hold a non-participating royalty interest, overriding royalty interest, or another royalty variant with different rights. Knowing which type you have clarifies whether you have only income rights or also leasing, bonus, executive, or other mineral ownership rights.

Important

Mineral View can help you see production, revenue trends, and projected income for your minerals. For questions about your specific royalty decimal, what your lease permits in deductions, how your title was calculated, or what type of royalty interest you hold, consult a qualified landman or Texas oil and gas attorney.

Common Questions

Generally no. A royalty interest is cost-free with respect to drilling, completion, operating, workover, and plugging costs under a standard lease. Those costs are borne by the working interest owners. The main thing to watch is post-production costs, such as gathering, compression, dehydration, treating, processing, transportation, and marketing-related charges, which some leases may allow to be deducted from your share. Those are different from drilling and operating costs, which royalty owners generally do not pay.

You hold a royalty interest, which generally means a share of production revenue without responsibility for drilling, operating, or controlling the well. The working interest owners bear the costs and control the economic side of the well, while the operator manages operations. A working interest owner's net share of revenue after royalty burdens is often described as net revenue interest. In short, you share in the revenue, while the working interest owners carry the costs and the operator manages day-to-day operations.

Generally not while your current lease remains validly in force. The royalty fraction is set in the lease, and as long as that lease remains validly in force, including while it is held by production, the fraction usually stays fixed unless the lease is amended. A different rate typically requires a new lease or amendment, and a new lease usually becomes possible only after the existing lease ends or releases the relevant rights.